Agentic AI for Financial Services Market Trends: Fraud Prevention, Cloud Deployment,

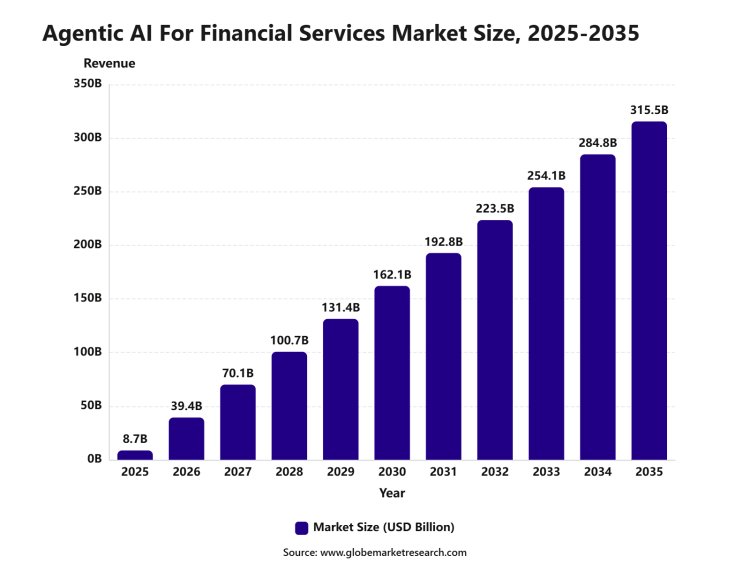

The Agentic AI for Financial Services Market was worth USD 8.7 billion in 2025 and is expected to reach approximately USD 315.5 billion by 2035, growing at a CAGR of 43.2% from 2025 to 2035

Share this Post to earn Money ( Upto ₹100 per 1000 Views )

According to Globe Market Research, the global Agentic AI for Financial Services Market was worth USD 8.7 billion in 2025 and is expected to reach USD 315.5 billion by 2035, growing at a CAGR of 43.2% from 2025 to 2035. North America led the market with a 40.3% share in 2025, supported by strong banking technology investment, mature cloud infrastructure, a large fintech ecosystem, and early adoption of AI in fraud prevention, risk management, customer service, and financial compliance.

Agentic AI for financial services refers to autonomous or semi-autonomous AI systems that can understand objectives, plan tasks, access approved tools, analyse financial information, and complete multi-step workflows with limited supervision. These systems are being applied across banking, insurance, payments, lending, capital markets, wealth management, financial crime prevention, and regulatory operations.

Unlike basic chatbots, agentic AI systems can connect with transaction databases, customer relationship platforms, risk engines, payment networks, document management tools, and compliance systems. They can collect information, recommend actions, initiate approved processes, and escalate higher-risk decisions to employees.

The technology is moving from experimentation into controlled enterprise deployment. In a 2026 financial services survey, 42% of respondents said their organisations were using or assessing agentic AI, while 21% had already deployed AI agents. Around 65% said their companies were actively using AI, compared with 45% in the previous survey.

Why the Agentic AI for Financial Services Market Is Growing

The growth of the Agentic AI for Financial Services Market can be attributed to rising fraud losses, higher digital transaction volumes, strict compliance requirements, and pressure to reduce manual work. Financial institutions must review millions of transactions, customer documents, risk signals, service requests, and regulatory records while maintaining accuracy and accountability.

Fraud prevention has become an important investment priority. The U.S. Federal Trade Commission received 3 million fraud reports in 2025, with reported consumer losses reaching USD 15.9 billion. Investment scams accounted for USD 7.9 billion, while imposter scams resulted in more than USD 3.5 billion in reported losses.

Payment fraud is also increasing in other major financial markets. UK Finance reported that criminals stole GBP 1.28 billion through payment fraud during 2025, representing a 4% annual increase. Around 66% of authorised push payment fraud cases started online, showing the need for stronger cross-platform monitoring and real-time intervention.

AI investment is producing measurable financial results. In NVIDIA’s 2026 financial services survey, 89% of respondents said AI had increased annual revenue or reduced annual costs. Around 64% reported revenue gains of more than 5%, while 61% achieved cost reductions above 5%.

Customer expectations are also encouraging adoption. A global survey of 9,500 financial-services consumers found that fewer than half were fully satisfied with their banks, insurers, or wealth management providers. Around 46% said they would remain with a provider offering excellent customer service even if rates or fees increased.

Fraud Detection and Anti-Money Laundering Lead the Application Segment

Fraud detection and anti-money laundering accounted for 30.5% of the Agentic AI for Financial Services Market by application in 2025. The segment is supported by rising digital fraud, synthetic identities, account takeover, transaction laundering, payment scams, and regulatory reporting requirements.

Agentic AI can monitor transaction patterns, compare customer behaviour with historical records, identify unusual account activity, retrieve supporting information, and prepare investigation summaries. High-risk cases can then be escalated to fraud analysts or compliance officers for approval.

These systems can also coordinate multiple fraud prevention steps. One agent may examine transaction history, another may check device or location information, and a separate compliance agent may review sanctions or customer-risk records. The findings can be combined into one structured case file.

The financial impact is becoming more important as fraud techniques develop. AI-supported fraud systems can reduce the time between detecting suspicious activity and taking action. Immediate intervention is valuable because delayed responses can allow funds to move across several accounts or jurisdictions.

Public authorities also recognise the role of advanced analytics in financial crime prevention. The Financial Action Task Force has stated that technology can improve the speed, quality, and efficiency of anti-money laundering and counter-terrorist financing measures. Data pooling and collaborative analytics can help financial institutions identify risk patterns more effectively.

Fraud detection and AML are expected to remain leading applications because they provide measurable financial value. Banks can track avoided losses, reduced false positives, shorter investigation times, improved case prioritisation, and lower compliance workloads.

Solutions Hold the Largest Component Share

Solutions accounted for 64.4% of the market by component in 2025. This category includes agent platforms, fraud detection engines, compliance automation tools, financial service assistants, risk analysis systems, workflow orchestration software, credit decision tools, and investment research agents.

The segment is being supported by demand for ready-to-deploy systems that can connect with existing financial infrastructure. Banks generally require platforms that can operate with core banking systems, customer data platforms, payment networks, document repositories, and regulatory databases.

Pre-built financial workflows can shorten implementation periods. Instead of developing every process internally, institutions can configure agents for activities such as customer onboarding, fraud investigations, service requests, credit document analysis, claims review, and regulatory reporting.

Solutions are also gaining demand because financial institutions need centralised governance. Enterprise platforms can provide user permissions, activity logs, approval rules, model monitoring, data controls, and escalation procedures within one operating environment.

Salesforce introduced Agentforce for Financial Services in May 2025 with pre-built agents for retail banking, financial advisory, banking service support, meeting preparation, and process compliance. The offering was designed to work with industry-specific financial data models and established workflows.

Services will remain important because financial institutions often require integration, model testing, cybersecurity assessment, data preparation, workflow redesign, compliance validation, and employee training. However, solutions are expected to retain their leadership as reusable financial agents become more widely available.

Cloud Deployment Leads the Market

Cloud deployments held 71.2% of the Agentic AI for Financial Services Market in 2025. Cloud infrastructure supports scalable computing, centralised data access, faster agent deployment, API-based integration, model management, and real-time financial analytics.

Agentic AI systems can require considerable computing capacity because they may use several models, tools, databases, and verification processes during one workflow. Cloud platforms allow financial institutions to expand computing resources according to transaction volume and application demand.

Cloud deployment also supports faster development. Banks and insurers can use managed AI services, secure model hosting, document processing, data warehouses, monitoring tools, and agent development frameworks without building each technical layer independently.

Google launched its Gemini Enterprise Agent Platform in April 2026 to help organisations build, connect, deploy, govern, and optimise AI agents. The platform combines model access, agent development, integration, security, orchestration, and operational management.

Cloud adoption does not remove the need for data controls. Financial institutions must determine which information can be processed in public cloud environments, private cloud infrastructure, on-premise systems, or controlled hybrid environments.

Hybrid deployment is therefore expected to remain important for sensitive workloads. Customer records, payment information, trading data, and regulatory documents may remain within controlled systems while cloud-based agents perform permitted tasks through secure connections.

Commercial Banks Are the Leading End Users

Commercial banks accounted for 47.8% of the market by end user in 2025. Their leadership is supported by large transaction volumes, broad customer bases, complex regulatory obligations, extensive service operations, and strong demand for fraud prevention and workflow automation.

Agentic AI can be used across retail banking, commercial banking, payments, lending, treasury, compliance, customer service, and internal operations. Banks can deploy agents to answer routine questions, prepare customer meeting information, monitor accounts, analyse lending documents, and assist fraud investigators.

Bank of America reported in April 2025 that more than 90% of its employees were using its internal Erica assistant. The tool reduced calls to the bank’s IT service desk by over 50%, while generative AI coding assistance produced efficiency gains above 20% for software developers.

The bank also reported that Erica had exceeded 3 billion customer interactions by August 2025 and was averaging more than 58 million interactions each month. This level of usage demonstrates the potential scale of AI-supported banking services when tools are integrated into established customer channels.

Commercial banks are also investing in employee-facing agents. Bank of America’s AskGPS assistant was trained on more than 3,200 internal documents and was introduced to help teams serve over 40,000 business clients. Questions that previously required up to an hour could be answered within seconds.

Investment banks and asset managers represent another important opportunity. Agentic AI can support financial research, document review, portfolio monitoring, market analysis, due diligence, risk reporting, and investment meeting preparation.

Insurance companies can use agents for claims intake, policy servicing, fraud screening, underwriting support, customer communication, and document classification. Fintech companies and digital banks may adopt faster because they generally operate with newer cloud-based infrastructure and fewer legacy systems.

North America Leads the Agentic AI for Financial Services Market

North America captured 40.3% of the global market in 2025. The region benefits from a large financial sector, mature cloud infrastructure, strong AI development capabilities, significant cybersecurity investment, and early adoption among commercial banks, payment companies, insurers, and asset managers.

The United States remains the main regional contributor because its leading financial institutions invest heavily in technology. Bank of America reported annual technology spending of approximately USD 13.5 billion in 2026, including about USD 4 billion for new initiatives such as AI.

BNY has also expanded enterprise AI adoption. By December 2025, its internal platform supported more than 125 live use cases, while 20,000 employees were actively building AI agents. The company reported that one legal workflow reduced review time by 75%.

Europe is expected to record strong demand as banks respond to digital transformation and responsible AI requirements. The European Union’s AI framework requires risk assessment, high-quality data, activity logging, technical documentation, human oversight, cybersecurity, and accuracy for systems classified as high risk.

UK financial institutions have already established a broad AI base. A Bank of England and Financial Conduct Authority survey found that 75% of responding financial firms were using AI, while another 10% planned to adopt it within three years. Respondents expected their median number of AI use cases to rise from nine to 21.

Asia Pacific is gaining momentum through digital banking, mobile payments, fintech growth, and financial inclusion initiatives. Banks in India, Singapore, Japan, South Korea, Australia, and Southeast Asia are expected to expand agent use across customer service, compliance, credit assessment, payments, and fraud prevention.

Go-to-Market Strategy for Agentic AI Providers

A strong go-to-market strategy should focus on commercial banks, insurers, payment companies, asset managers, investment banks, fintech firms, and compliance organisations. Each customer group should be approached with specific use cases rather than a general AI platform message.

Financial institutions do not purchase agentic AI only because it is an advanced technology. They require evidence that it can reduce fraud losses, shorten processing times, lower service costs, improve employee productivity, or support better customer outcomes.

Initial sales should focus on controlled workflows with measurable performance indicators. Suitable starting points include customer-service assistance, document summarisation, employee knowledge search, fraud case preparation, meeting preparation, compliance document review, and transaction inquiry management.

Pilot projects should include clear baseline measurements. Vendors should compare processing time, manual effort, false-positive rates, customer response time, case resolution rates, and cost per transaction before and after deployment.

Bank of America’s CashPro Search provides an example of measurable financial service automation. Early adopters reported a 20% reduction in telephone and email inquiries, while its AI-supported CashPro Chat achieved a 43% containment rate during the third quarter of 2025.

Sales models should combine software subscriptions, usage-based charges, integration services, governance tools, and ongoing model monitoring. Financial institutions may prefer phased contracts that begin with a limited workflow and expand after risk and performance requirements have been achieved.

Partnerships with cloud providers, core banking vendors, consulting firms, system integrators, and cybersecurity specialists can improve market access. These partners already have relationships with financial institutions and understand their technical and regulatory requirements.

Revenue Potential and Financial Impact

Revenue potential is strongest in fraud prevention, customer support, compliance automation, credit assessment, wealth management, financial research, claims handling, treasury operations, and document processing.

Fraud detection agents can create recurring revenue through transaction monitoring, investigation management, identity verification, alert prioritisation, sanctions screening, and continuous customer-risk assessment.

Customer-service agents can support account inquiries, payment tracking, dispute handling, card servicing, onboarding, appointment scheduling, and product information. Customer-related use of generative AI in financial services increased from 25% to 60% within one year, according to NVIDIA.

Treasury and cash-management workflows also offer commercial potential. In 2025, more than 3,000 companies using Bank of America’s CashPro Forecasting solution saved a combined 250,000 hours. An updated model introduced during the year processed and interpreted data five times faster.

Payment operations may become another major opportunity. Experiments published by the Bank for International Settlements found that an AI agent could maintain liquidity buffers, prioritise urgent payments, and balance settlement delays against liquidity costs in simulated payment scenarios.

The financial impact for customers will depend on workflow volume, labour intensity, risk exposure, integration cost, and accuracy. High-volume activities such as transaction monitoring, customer inquiries, claims processing, and document review are likely to produce clearer returns than low-volume specialised processes.

Revenue can also be generated through governance and monitoring. Banks will need tools that record agent actions, identify unusual behaviour, control system access, test performance, manage model changes, and generate audit evidence.

Risk Factors and Market Barriers

Regulation and accountability remain major barriers. Financial institutions must be able to explain how customer information was used, which systems were accessed, what action was recommended, and who approved the final decision.

Agentic systems create additional risk because they can take actions instead of only producing text. Poorly controlled agents could retrieve unauthorised information, initiate incorrect transactions, provide unsuitable advice, or make inconsistent compliance decisions.

The Bank for International Settlements has identified model risk, data quality, limited explainability, cloud concentration, cyber vulnerabilities, and dependence on a small number of technology providers as important financial stability concerns.

Data quality is another barrier. Financial information is often distributed across legacy systems, regional databases, customer platforms, archived documents, and third-party providers. Agents may produce incomplete or incorrect results when information is outdated, duplicated, or poorly structured.

Cybersecurity risk is also increasing. AI may help financial institutions detect attacks, but criminals can use the same technology to create synthetic identities, deepfake communications, personalised scams, malicious code, or automated social engineering campaigns.

Financial institutions must also prevent excessive autonomy. Lending decisions, investment recommendations, fraud account closures, claims denials, and regulatory filings require clear approval rules and human review.

Implementation costs can be significant. Expenses may include cloud infrastructure, AI models, data preparation, system integration, employee training, cybersecurity testing, compliance assessment, and ongoing performance monitoring.

Key Opportunities in the Agentic AI for Financial Services Market

The strongest opportunity is fraud detection and AML automation. Growing fraud losses are encouraging banks to adopt systems that can monitor transactions continuously, investigate unusual activity, prepare case summaries, and recommend appropriate responses.

Personalised banking is another important opportunity. Agents can analyse account activity, customer goals, service history, and approved financial information to provide relevant guidance or direct customers to appropriate products and employees.

Customer-service automation is gaining momentum because financial institutions must support customers across mobile applications, websites, telephone channels, email, and messaging platforms. AI agents can provide 24-hour assistance while transferring complex or sensitive cases to employees.

Credit assessment agents can help collect application documents, verify information, review financial statements, calculate risk indicators, and prepare decision summaries. Final lending decisions should remain subject to established policies and human oversight.

Wealth management agents can assist advisors with meeting preparation, portfolio summaries, market information, customer communication, and administrative work. This allows advisors to dedicate more time to financial planning and client relationships.

Compliance agents represent a high-value enterprise opportunity. These systems can review policy changes, compare internal procedures with regulatory requirements, monitor employee activities, organise audit evidence, and alert compliance teams to possible issues.

Financial research agents can retrieve public filings, extract key information, compare companies, summarise earnings documents, and prepare structured analysis. Platforms such as Endex are developing autonomous financial analysts that connect internal information with public disclosures and trusted financial sources.

Analyst Perspective: What the Data Is Telling Financial Services Companies

The data indicates that financial services organisations are moving beyond basic chatbot deployment. AI agents are increasingly being connected with real banking, payment, compliance, and investment workflows.

The strongest signal is the combination of a 30.5% share for fraud detection and AML, a 64.4% share for solutions, a 71.2% share for cloud deployment, and a 47.8% share for commercial banks. These indicators show that buyers are prioritising scalable platforms that address measurable operational and risk-management problems.

The transition will remain controlled rather than fully autonomous. Financial institutions will adopt agents faster in activities where permissions, decisions, and escalation procedures can be clearly defined.

What Opportunities Are Emerging?

Fraud prevention is expected to remain the largest near-term opportunity because institutions can measure avoided losses, investigation speed, false-positive reduction, and employee productivity.

Internal financial agents also provide strong potential. Employee knowledge search, document preparation, software development, compliance support, and client meeting preparation can improve efficiency without immediately transferring sensitive decisions to machines.

Multi-agent systems are emerging for complex workflows. Separate agents may be used for identity verification, customer-risk assessment, document review, transaction analysis, and compliance reporting within one controlled process.

What Risks Should Companies Be Aware Of?

The main risk is allowing agents to act without appropriate limits. Every system should have defined access permissions, financial thresholds, approval requirements, audit logs, and exception procedures.

Model concentration is another concern. If many financial institutions use similar models, cloud providers, and data sources, a common technical failure could affect several institutions at the same time.

Companies must also manage bias and explainability. Credit, insurance, fraud, and investment decisions can affect customers significantly, making data quality, testing, documentation, and human review essential.

What Decisions Should Clients Make Next?

Clients should identify a small number of high-volume workflows with measurable costs and clearly defined decision boundaries. Fraud case preparation, customer inquiries, compliance searches, and document review are practical starting areas.

A governance structure should be established before wider deployment. Responsibility for agent approval, data access, cybersecurity, model validation, performance monitoring, and incident management should be clearly assigned.

Explore More Reports

- https://www.globemarketresearch.com/reports/agentic-ai-for-financial-services-market

- https://www.globemarketresearch.com/reports/nuclear-fusion-market

- https://www.globemarketresearch.com/reports/hydrogen-fuel-cells-market

- https://www.globemarketresearch.com/reports/single-phase-string-inverters-market

- https://www.globemarketresearch.com/reports/power-generation-market

- https://www.globemarketresearch.com/reports/hydropower-generation-market

- https://www.globemarketresearch.com/reports/cloud-computing-market

- https://www.globemarketresearch.com/reports/ai-visual-inspection-system-market

![Ever Joint Canada – [Must Read] Powerful Joint Support Backed by Science](https://blog.rackons.in/uploads/images/202509/image_380x226_68c50d7a82a7b.jpg)